Private equity funds (also referred to as PE or sponsors) have rapidly and dramatically entered the carwash space over the last five years. In 2016, only two of the top 10 carwash chains (in terms of the number of sites operated) were owned or backed by private equity. Today, all 10 are.

The average number of sites among the top 10 has increased from 51 to 213. The percentage of all conveyor washes in the U.S. operated by the top 10 has gone from 3% to 12%. When this wave of consolidation started in earnest, large transactions were funded in part by equity (both from the PE shop and often existing management who would retain some ownership) but in large part by debt.

Banks and direct lenders were not only more than willing to finance just the original purchase, but they would also build in flexibility that allowed PE firms to have ready access to capital to further expand through greenfield or acquisition. These loans are priced as a spread above Secured Overnight Financing Rate (SOFR), and the interest rate floats with SOFR. While the spreads over SOFR have stayed relatively constant (around 5% to 6%), SOFR itself has risen from basically 0% to 5.1% today. That means financing rates have doubled in less than a year. As you can imagine, this has had a dramatic impact on the industry, and that impact will probably continue well into the future.

To understand the impact, it is worth examining how PE shops get paid. I am writing in generalities, as there are different types of PE funds with different goals, but am focusing on the most common arrangements. The sponsor is most often paid in two ways. First, it receives a management fee of roughly 2% of committed capital annually. This stream keeps the lights burning. Second, it receives a carry of roughly 20% of the profit of a portfolio company once the original capital and a preference (usually around 6% to 8%) have been returned to the investors. This carried interest is meant to be the far more lucrative piece of overall PE compensation.

The success of a fund is measured both in terms of IRR (an annualized percentage return for the life of an investment) and the Multiple of Invested Capital (MOIC). The more successful a fund is, the more likely the sponsors will be able to raise a new, larger fund and the more money they can make.

This arrangement drives certain behaviors. In order to enjoy the benefit of the carried interest and in order to allow PE shops to raise new funds, they must deploy capital. Sitting on a pile of cash, even in challenging times such as ours, defeats the basic goals of PE. Additionally, there is an incentive to use as much debt as is reasonably possible. The less equity that is used to fund a project, the greater the returns to the equity holders if it is successful. Adding more equity as an investment ages can be damaging to IRR, which is an important measure of success.

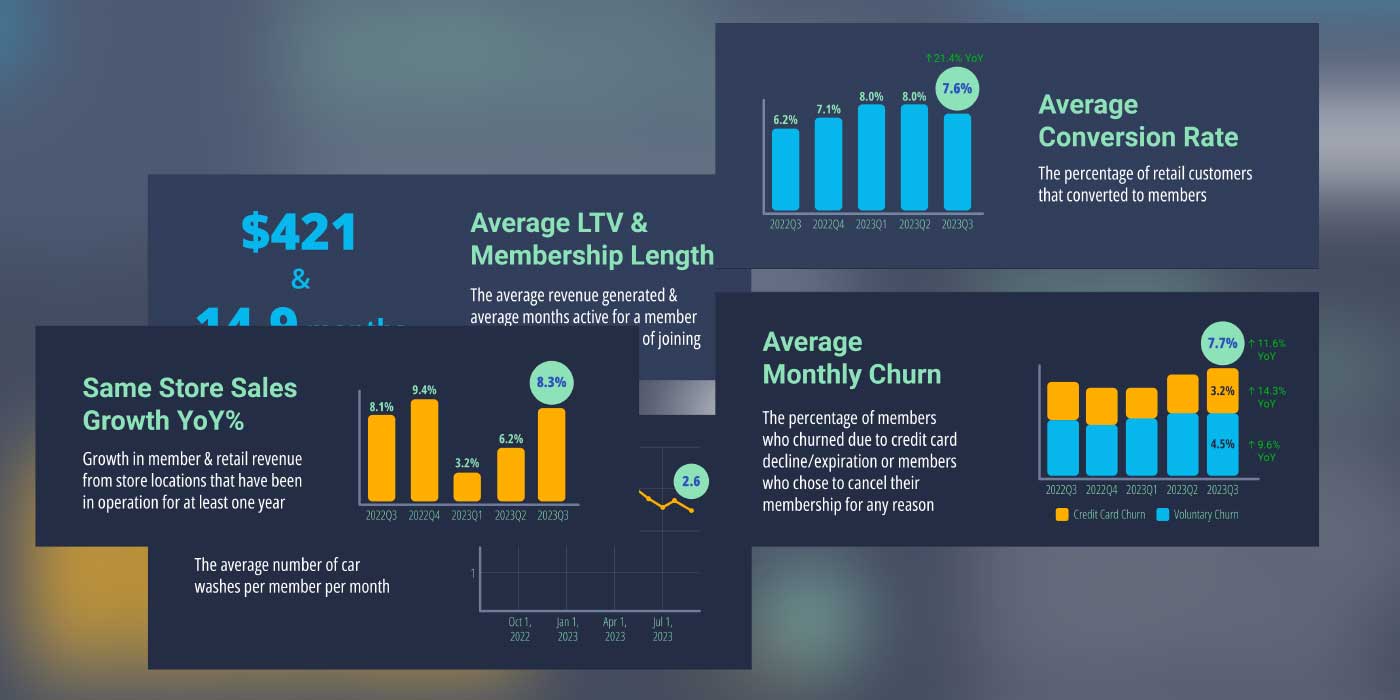

Also, there is a tremendous incentive to continue investing in the platform company, particularly using debt capital. A larger business can enjoy economies of scale in operations, financing and exit. Typically, a larger chain will sell for a higher multiple. When you take valuation to its core, it is based on EBITDA (earnings before interest, taxes, depreciation and amortization) times a multiple. EBITDA is raised through more efficient operations, more revenue through tools such as membership programs and more sites. Multiples go up with the size of a chain as well as the quality of management, average profitability per site and a myriad of other factors. PE focuses on each of these elements.

Finally, a PE shop will focus on a hold period of three to seven years. This gives it enough time to make meaningful changes and grow materially. It does tend to tip the scales to growth through acquisition rather than greenfield, as the benefits can be seen much more quickly. To summarize, PE wants to deploy cash, use as little equity and as much debt as practical, grow aggressively and exit in the near term.

So that was a lot of information in just a few paragraphs, but below I have tried to capture how PE has reacted to this challenging financing market and how the four basic PE behaviors have influenced our industry.

• The reality is that there were several large carwash chains on the market last year, and most did not find buyers. Acquisition multiples have fallen since the highs of early and mid-2022 — in many cases dramatically. Sites are far more difficult to sell, and buyers are far more reluctant to pay up, even for great assets. Sellers, for their part, still remember the good old days and aren’t willing to sell at prevailing prices. The important thing to note is that buyers aren’t being irrational in forcing prices down. Debt capital is not just more expensive — it’s tougher to get. Doubling the debt rate forces buyers to lower their prices or to accept a much lower return on their investment, which they are not going to do.

• In a market where mergers and acquisitions (M&A) are rarer as buyer and seller expectations diverge, the need to grow and deploy cash has necessarily moved the focus of carwash operators to greenfield development. Greenfield has the disadvantage of taking far more time than M&A to make an impact on the bottom line, but historically has had the advantage of being more cost-effective and can often be largely debt-financed. Although acquisitions of one-off sites or small chains are happening with less frequency, they still occur and are likely to become once again more common, particularly as sellers become more realistic in their expectations.

• Traditional lenders have soured on the carwash market. Many of the large transactions completed over the last few years had a number of lenders in common. This group found the space very compelling and aggressively pursued transactions where they could put their capital to work. The dramatic move in interest rates has made the credit statistics of borrowers weaker, and that go-to group of lenders has understandably become more skeptical when there is a request for a loan. This has led to more creative financing alternatives.

• Sale leasebacks have continued to gain momentum as a source of financing. If you enter into a sale leaseback, you sell your land and building to a third party who then becomes your landlord. The rent you pay is a percentage of the price you are given for the upfront sale (the cap rate). Cap rates are around 7% today and have not changed dramatically even in the face of the massive hike in interest rates. That means they are relatively more attractive today and a powerful tool in avoiding equity infusions.

• Some groups are suffering financial hardship. If you buy a chain of carwashes and factor in interest rate coverage of two times, you are being reasonably prudent. If six months later the operation is generating the same cash flow, but the interest burden has doubled with the rate increases, you are now using all your available cash flow to make interest payments. There is no money for growth.

• A different group of buyers is looking to enter the space. As current owners work through debt and greenfield issues, other buyers are taking more interest. The purchase by Circle K of True Blue is just one example. Also, wealthy individuals are looking to buy small chains as a way of diversifying into an attractive market.

• Even as growth has become more dependent on greenfield development, sites have become significantly more expensive to build because land, construction and equipment costs have risen dramatically. Also, municipalities are taking longer to work through the approval process. This hampers growth and will likely drive PE back to acquiring operational sites.

• Competition has increased, in some cases dramatically. The need for growth and capital deployment has led to a wave of development. The days where competitors were careful not to encroach on a neighboring wash are over.

• Carwash is still a great place to invest. There is more competition in many markets, but in a large number of cases, that seems to have only made the pie bigger in terms of customers served. Margins for express washes are high, and revenue has been smoothed with the advent of the monthly pass program.

So, the carwash world is still a great one. Interest rates will sort themselves out, and transactions will start back up, but things won’t be entirely the same. Let’s make some predictions.

• Valuation multiples will not recover all the way to where they were before. Things will get better, capital will loosen up, but I believe the feeding frenzy of late 2021 and early 2022 is over.

• Mergers will lead to a handful of superchains. The biggest firms in the space will pair up, as has happened with so many consolidating industries in the past. These chains will have unprecedented access to capital and will enjoy meaningful economies of scale that have the potential to lead to a compelling public equity story. I guess there will be five or six public chains, each with at least 500 sites.

• Mom-and-pop chains will continue to feel the heat. As competition increases and chains get larger, existing small groups will find it harder to thrive. Some will thrive, particularly those with highly defensible geographies, but it’s only going to get tougher.

• Municipalities will get tired of letting more carwashes get built in their jurisdictions. I see this anecdotally already but feel like in the more crowded geographies, it will accelerate. Additionally, concerns over noise pollution and water usage will continue to grow in importance.

• The industry will become more efficient. Prices for washes have gone up across the board, and that has driven profits higher. Ultimately, with enhanced competition, that tool will be less impactful, and efficiencies in operations and superior service offerings will have to be found to extract value. Things such as smaller footprints, fewer employees and greater energy efficiency are just a few possibilities.

The impact of PE on carwash is a complex topic, and this article just starts the conversation. Ultimately, it is neither good nor bad overall, but it will drive winners and losers. PE buyers provide an efficient market for sellers. They dramatically increase the pool of potential acquirers, which leads to more successful transactions at higher average prices. On the other hand, they potentially harm washes whose owners do not wish to sell by building high-quality competition. The good news is that their intentions are clear and understandable, which makes most of their moves predictable and based on sound business motivation. It’s how we respond that matters.

George Odden is a partner at Ardent Advisory Group.